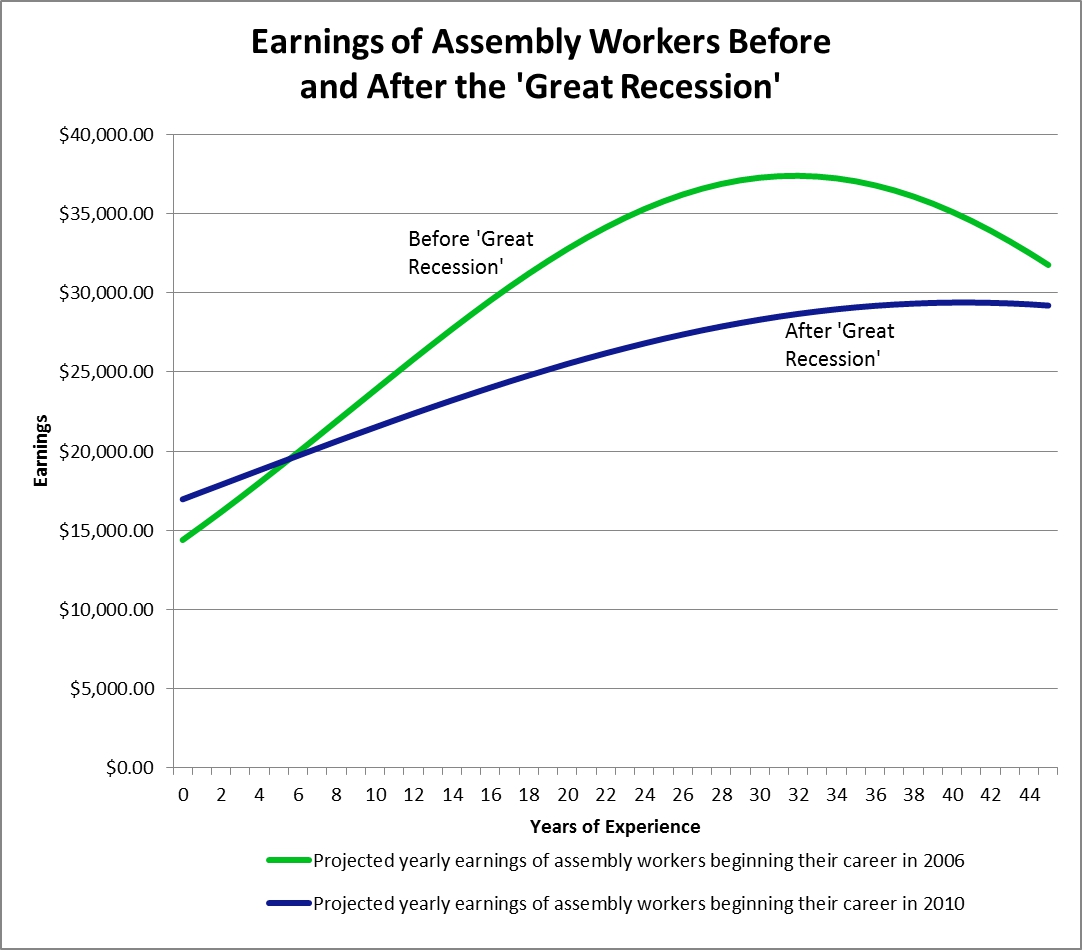

A person’s earnings will tend to increase as they age…to a certain point. After that point, which is around age 46 or so depending on the person’s education level and occupation, the person’s earnings will tend to decrease as the age.

The age-earnings profile captures this phenomenon. The age-earnings profile is calculated from data sources like the Current Population Survey from the U.S. BLS

Here is a question that we recently addressed:

Q: Any idea on how to create an age-earnings profile for someone specifically with an MBA? Are there data somewhere that have created such a profile? I can see using the ACS (American Community Survey) to look at people by age who have a master’s degree and are employed in management occupations. Anything more specific?

A: The ACS would be a good start and would allow you to estimate an age-earnings profile more specific to the facts in your case. In our cases we generally estimate the age earnings profiling using a regression model. In our cases, there are generally not enough observations to filter for all the specific facts that we want to account for so a regression approach has been useful for us.

Standard age earnings profile regressions from labor economics models, see for example papers by Mincer et al., Lazear et al, , Welch et al. and many more, regress earnings on experience, experience squared, occupation variables, geographical variables, and education variables.