A recent article in the New York Times explored the brewing debate concerning the current U.S, ban on exporting oil outside of the U.S.

In a nutshell, the producers want to export oil while the refiners want to keep the oil in the US

The refiners: The refiners want to keep the oil in the US so they have more oil to refine. Keeping the oil in the U.S. also keeps refining competition from abroad in check.

Keeping the export ban would possibly lower prices for oil and gas products, refiners argue. To refiners exporting oil cuts into their bottom line.

Oil producers: On the other side of the equation the oil producers are concerned that having the restriction to only selling the United States will eventually lower their profits by reducing the price of crude oil in the U.S.

Natural gas in the price of natural gas has seen that same type of phenomena over the last decade as Shale and hydro-fracturing has led to much lower natural gas prices in the US

The concern among oil producers is that the lower price (that results from the export ban) would eventually cut into their bottom line as more and more crude oil is put on the market with the new discoveries in South Texas and other places in the United States

In the long run producers are concerned that there would be an exit of producers and or a reduction of new finds in the United States. Since the price that they would receive for crude oil would be lower.

The natural gas market is a good example of the potential impact that crude oil producer see. The natural gas industry faced and continues to face lower prices in part due to the fact that it is not as easy to export natural gas. As a result of not being able to export natural gas readily from United States the large number of hydro-fracturing finds in the United States have stayed in United States. As a result the price of natural gas products has fallen. That is clearly the concern that is clearly the concern of the crude oil producers in United States.

Data released by the credit giant TransUnion indicates that :

Data released by the credit giant TransUnion indicates that : Austin American Statesman reports

Austin American Statesman reports The New York Fed surveys over 1,500 small firms twice a year about their financing and credit needs. Responses to the Small Business Credit. (It would be nice for the other Fed banks to do a similar study, hint, hint)

The New York Fed surveys over 1,500 small firms twice a year about their financing and credit needs. Responses to the Small Business Credit. (It would be nice for the other Fed banks to do a similar study, hint, hint)

News about the Bitcoin the week of 12.20.2013

News about the Bitcoin the week of 12.20.2013 What is that loud sucking sound?

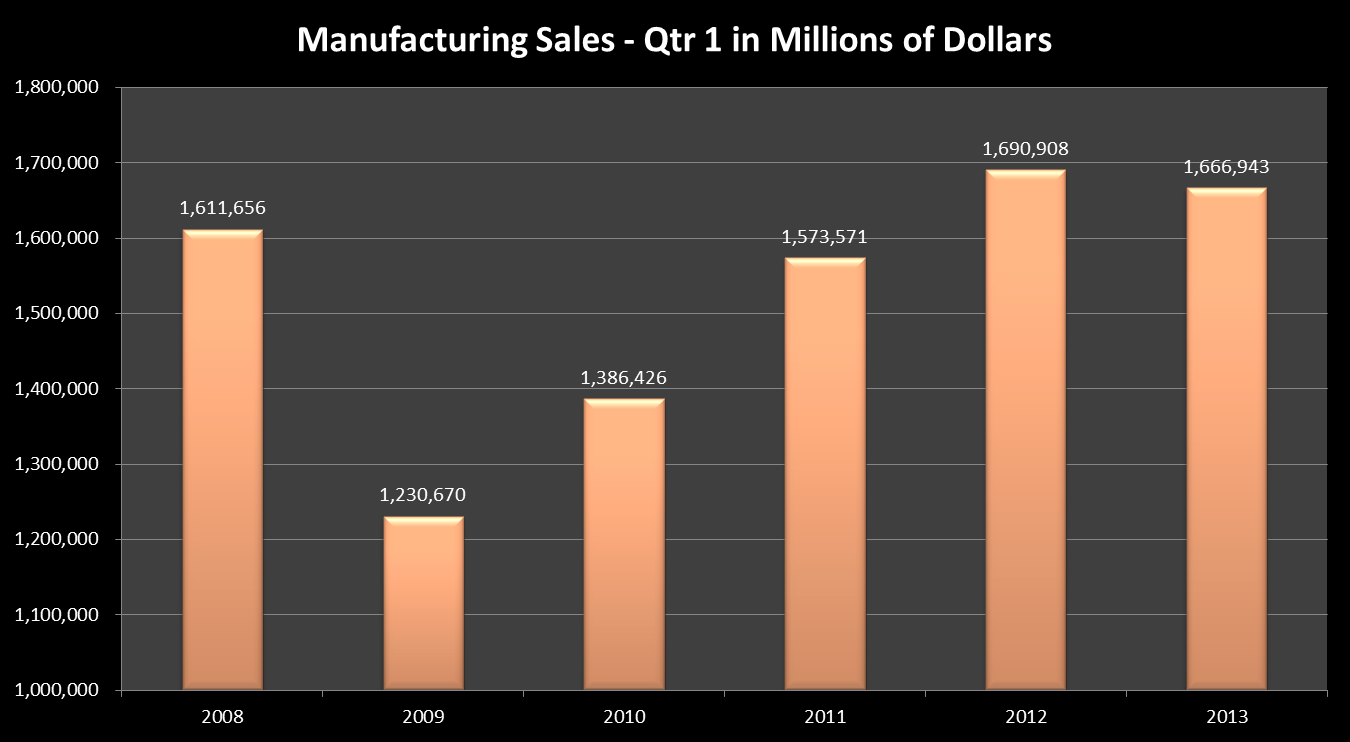

What is that loud sucking sound?  No matter what data you look at, manufacturing in the U.S. continues to increase. Sales for all U.S. manufacturers exceeded $1.69 trillion in the 1st quarter of 2012. In comparison, 1st quarter sales of manufacturing goods had falling to about $1.2 trillion at the deepest point of the ‘great recession’ in 2009.

No matter what data you look at, manufacturing in the U.S. continues to increase. Sales for all U.S. manufacturers exceeded $1.69 trillion in the 1st quarter of 2012. In comparison, 1st quarter sales of manufacturing goods had falling to about $1.2 trillion at the deepest point of the ‘great recession’ in 2009.