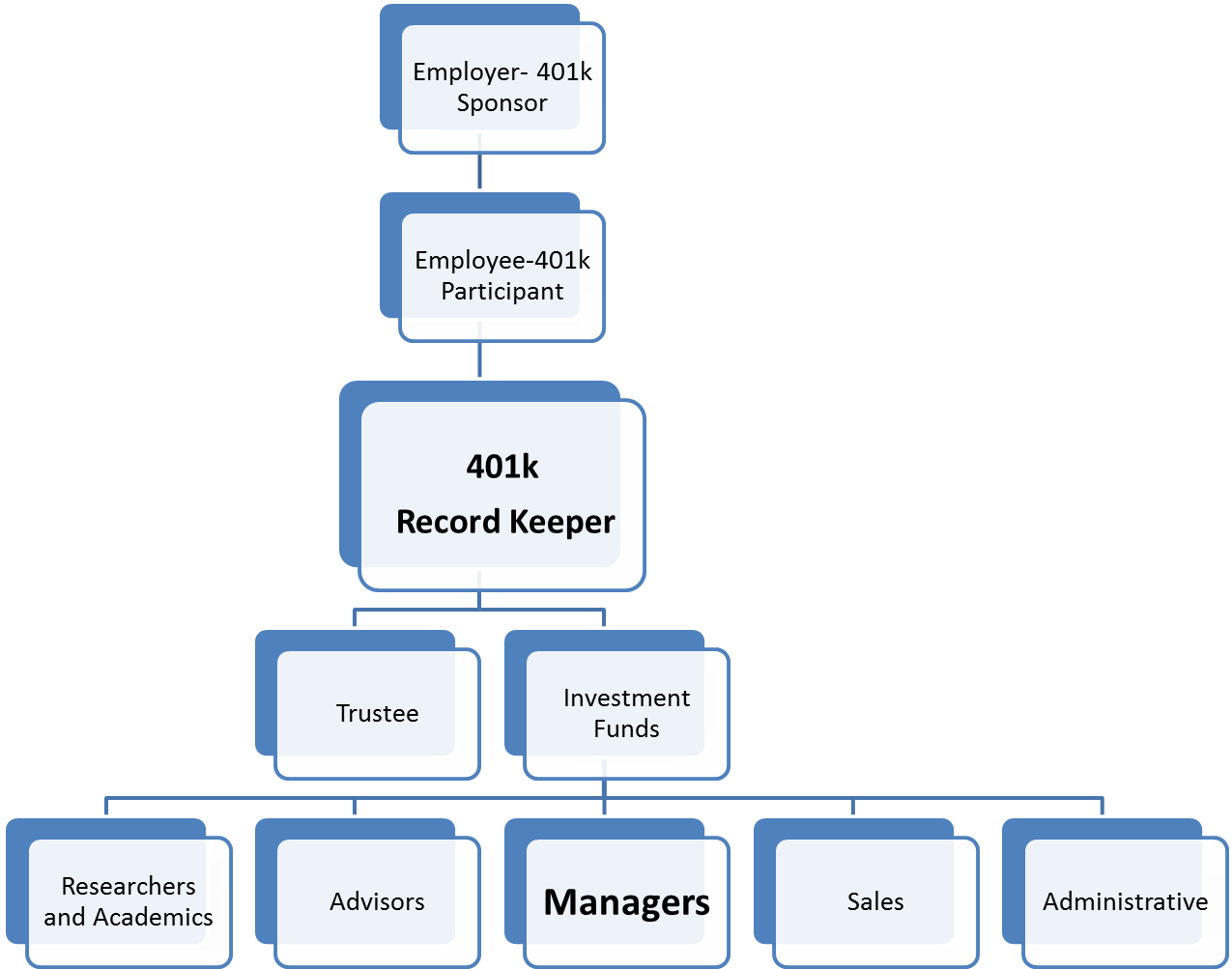

The players and how the relate to one another.

The players and how the relate to one another.

Author: Dwight Steward, Ph.D.

Dr. Steward regularly writes and speaks on topics involving business and individual economic damages, employment audits, and the analysis of payroll and time data in wage and hour investigations. Dr. Steward has also held teaching positions at The University of Texas-Austin in the Department of Economics and in the Red McCombs School of Business, The College of Business at Sam Houston State University, and at The University of Iowa. He has taught numerous courses in statistics, corporate finance, labor economics, business policies, managerial economics, and microeconomics.

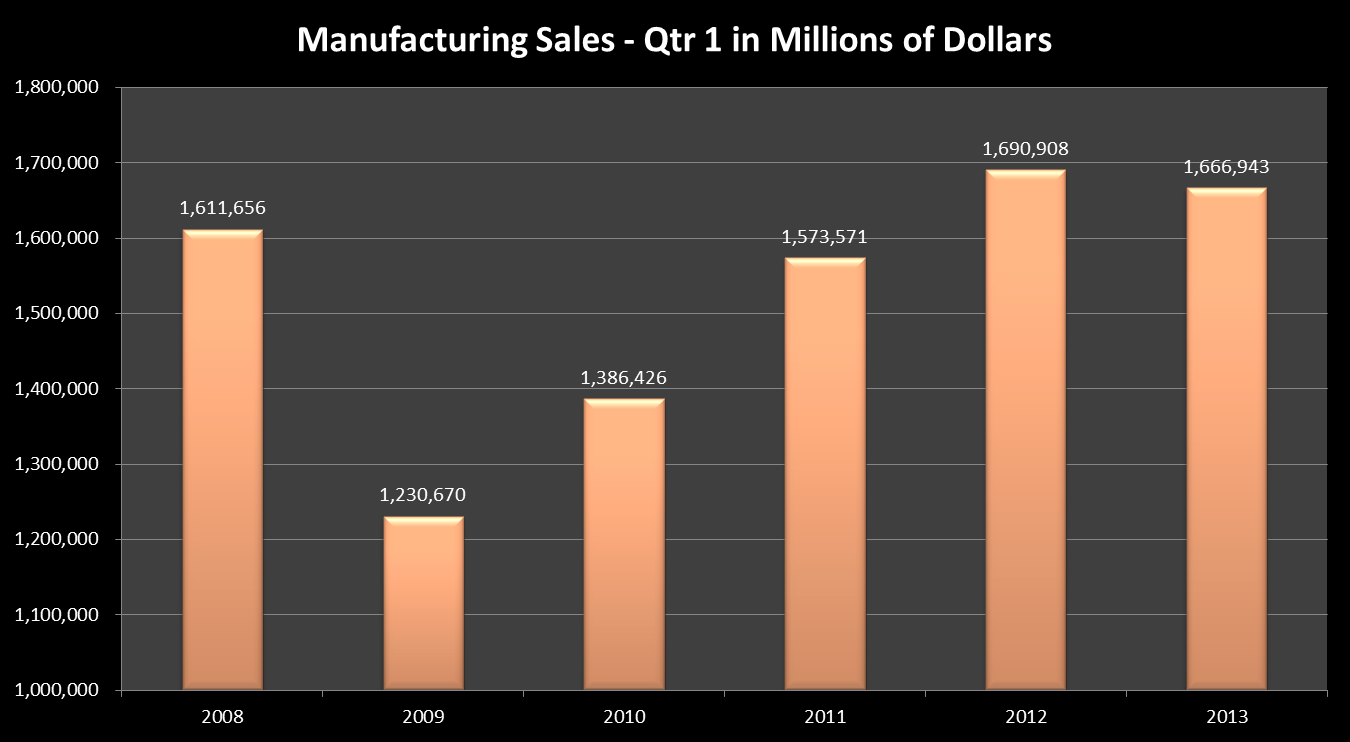

More and more things are being made here;U.S. Census data shows manufacturing in the U.S. (and Texas) continues to rebound

No matter what data you look at, manufacturing in the U.S. continues to increase. Sales for all U.S. manufacturers exceeded $1.69 trillion in the 1st quarter of 2012. In comparison, 1st quarter sales of manufacturing goods had falling to about $1.2 trillion at the deepest point of the ‘great recession’ in 2009.

No matter what data you look at, manufacturing in the U.S. continues to increase. Sales for all U.S. manufacturers exceeded $1.69 trillion in the 1st quarter of 2012. In comparison, 1st quarter sales of manufacturing goods had falling to about $1.2 trillion at the deepest point of the ‘great recession’ in 2009.

Manufacturing levels have reached, and slightly exceeded pre-recession economic output in nominal or non-inflation adjusted terms. Before the recession, manufacturing 1st quarter sales were at $1.6 trillion in nominal or non-inflation adjusted terms.

So where is a good source for manufacturing output information?

http://www.census.gov/econ/manufacturing.html

The U.S. Census industry portal is also a good source

http://www.census.gov/econ/isp/

Cyber-currency and the latest gold rush

The idea of a global cyber-currency is taking hold at least in some circles. Bitcoins, which is a digital fiat currency, has increased in value. On some exchanges the value of a single digital bitcoin currency has increased to over a $1,000.

The idea of a global cyber-currency is taking hold at least in some circles. Bitcoins, which is a digital fiat currency, has increased in value. On some exchanges the value of a single digital bitcoin currency has increased to over a $1,000.

So what is a bitcoin? According to the BBC World news , Bitcoin is a new kind of currency that ican be thought of as virtual tokens rather than physical coins or note. Like all currencies its value is determined by how much people are willing to exchange it for.

The bitcoin market is composed of miners, traders, and users of bitcoin. Like gold or commodity based currencies, miners discover new bitcoin. Bitcoin is mined using complex computer and mathematical algorithms. Like supplies of gold, the complexity of the mining process keeps the supply of bitcoin stable.

Currently there are about 11 million bitcoins in existence. Bitcoin transactions are anonymous and untracable. Sites like,spendbitcoin , provide lists of vendors that accept bitcoin. The vendors include internet services, manufacturing, and legal services.

Stacked employee ratings and performance bell-curves

Some employers grade their employee’s job performance on a curve. In these systems, like back in college, the employer generally sets the number of A, B,C’s etc. to assign to the employees performance. Proponents argue that the system is more fair and adds to employee moral in the long run. Neal Buethe of

Some employers grade their employee’s job performance on a curve. In these systems, like back in college, the employer generally sets the number of A, B,C’s etc. to assign to the employees performance. Proponents argue that the system is more fair and adds to employee moral in the long run. Neal Buethe of

Briggs and Morgan,

and

Nancy Gunzenhauser and Jeffrey Landes of Epstein Becker Green

discuss some of the legal issues to consider when adopting these types of systems.

Economist wades into climate change debate

William Nordhaus, a Yale economist studies the economics of climate change. Prof. Nordhaus’ work studies the inter-workings of climate change projections, pollution and global economic growth. He offers a number of projections and calculations of the trade-offs between taxes, climate change and economic growth.

William Nordhaus, a Yale economist studies the economics of climate change. Prof. Nordhaus’ work studies the inter-workings of climate change projections, pollution and global economic growth. He offers a number of projections and calculations of the trade-offs between taxes, climate change and economic growth.

Reviews of the book:

FLSA Regular Rate Calculations Accounting for Bonuses: Part 3 of 3.

Example #2—Nurse Retention bonuses (Part 3 of 3)

A health care organization’s nursing department gives hourly paid LPNs and RNs a $2,000 bonus after being employed for 6 months to both retain and attract more nursing personnel. In this instance, the bonus will be included in the regular rate calculation during weeks in the period in which overtime was worked. The key is to know how the bonus was earned. That is, was it a one time bonus? Or was it for work that was performed over a series of months. In this example is the latter.

The $2,000 retention bonus described above was earned over 6 months or 26 weeks. Equivalently, the weekly bonus can thought of as a weekly bonus of $76.92 ($2,000 ÷ 26 weeks). If an employee works overtime during the 26-week period, the increase in the regular rate is calculated by dividing $76.92 by the total hours worked during the overtime week.

The procedure for calculating OT is the same as described in Part 2 of this series. If the employee worked 10 hours of overtime ( a total of 50 hours of work in the pay period) in their 9th week of employment, the employee would be due an additional $7.70 in overtime earning in that time period. The calculation is as follows:

1. Calculate the increase in regular rate due to the bonus

$76.92 ($2,000 ÷ 26 weeks) ÷ 50 hours = $1.54 (increase in the regular rate)

Note: The daily bonus is spread equally of all the hours worked in the time period where there is OT.

2. Calculate the increase in the half time (.5) portion of the OT premium

$1.54 x ½ = $ .77 (increase in the additional half-time premium)

3. Calculate the addition OT premium due to the individual.

$ .77 x 10 hours of overtime worked = $7.70 (increase in overtime earnings due to the bonus)

The calculation can also be performed as described in yesterday’s post. The results will be the same. The key is to recognize that the bonus is spread over the time period that the bonus was earned.

Regular rate FLSA calculations accounting for bonuses: Part 1 of 3.

Excerpted from: Stephen Bruce PhD, PHR

Excerpted from: Stephen Bruce PhD, PHR

According to FLSA Overtime, at the rate of at least time and one half, must be paid on all hours worked over 40 in a workweek at the individual’s “regular rate,” not on the nominal hourly rate. FLSA requires that nondiscretionary bonuses must be included in the regular rate of pay. Non-discretionary bonuses include those that are announced to employees to encourage them to work more steadily, rapidly, or efficiently, and bonuses designed to encourage employees to remain with a facility.

The Department of Labor states that few bonuses are discretionary under the FLSA, and therefore few can be excluded from the regular rate.

So, to calculate the amount of the overtime premium, you must first adjust the pay to include the bonuses and then calculate the overtime premium. In practice, it’s often the case that you award bonuses after a paycheck has been issued, and in that situation, you must go back and recalculate the overtime and pay the difference. It’s usually a small amount, but it still must be paid. Referral bonuses paid for recruitment of new employees are not included in the regular rate of pay if they meet certain conditions (voluntary, not time intensive, after hours among friends and family).

The basics of Phantom Stock issues

What is it?: Phantom stock is a form of compensation where a company promises to pay cash at some future date, in an amount equal to the market value of a number of shares of its stock. The recipent does not receive actual stock.

What is it?: Phantom stock is a form of compensation where a company promises to pay cash at some future date, in an amount equal to the market value of a number of shares of its stock. The recipent does not receive actual stock.

How does it work? The payout on Phantom Stock will increase if the stock price rises, and decrease if the stock falls, but without the recipient actually receiving any stock. Like other forms of stock-based compensation plans, phantom stock broadly serves to encourage employee retention, and to align the interests of recipients and shareholders.

Phantom stock is essentially a cash bonus plan, although some plans pay out the benefits in the form of shares. Phantom stock is favored by closely held or family-owned companies who want to provide incentives to management and other employees without granting them equity.

How is it taxed? When the payout is made, it is taxed as ordinary income to the employee and is deductible to the employer. Generally, phantom plans require the employee to become vested, either through seniority or meeting a performance target.

Sources: The National Center of Employee Ownership, http://www.nceo.org/articles/phantom-stock-appreciation-rights-sars) http://en.wikipedia.org/wiki/Phantom_stock Pictures and images: http://slgsecurities.files.wordpress.com/2012/09/incentive-phantom-stock-michae_10762769.jpg

Dr. Sandra Black’s work on lifetime earnings and school starting age.

Dr. Sandra Black, UT-Austin economics professor, looks at the impact of school starting age and family background on work earnings. From her work:

We find that if you enter the labor market later, as a result you have less experience and so you get paid less than the people who are the same age who started earlier, but by age 30 you’ve caught up. – Dr. Sandra Black

Wage and hour case filings in Texas

| Year | FLSA cases filed in Texas |

| 2005 | 328 |

| 2006 | 262 |

| 2007 | 290 |

| 2008 | 350 |

| 2009 | 526 |

| 2010 | 644 |

| 2011 | 685 |

| 2012 | 632 |

| 2013 | 885 |

Jan. 1, 2005 to Oct. 28, 2013

Source: U.S. PACER database